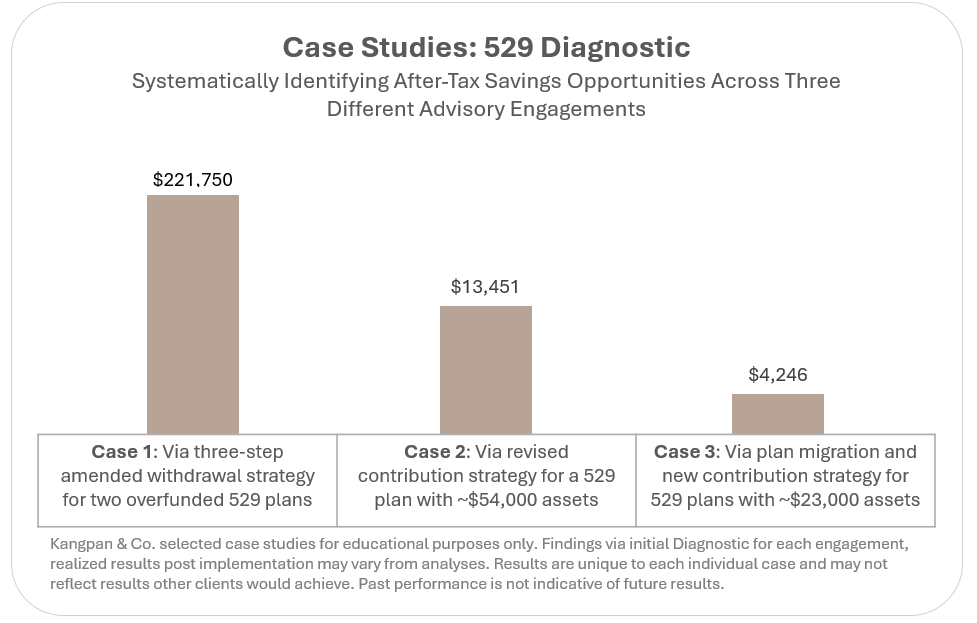

This post details our approach to optimizing a client’s college savings strategy using a Diagnostic. Check out our primer posts on Systematic Optimization and Diagnostics to learn more about our unique approach to financial advisory .

It’s common to wonder whether you’re saving enough for your children’s educational needs and to also be unsure what the tradeoffs are to being underfunded vs. overfunded. Our 529 Plan Diagnostic is designed to quickly give clear answers to these and other common questions while enabling us to provide a comprehensive, tailored recommendation for improving your overall approach to college savings.

As with all our Diagnostics, this structured approach ensures we are comprehensively examining your situation in a methodical way, quantifying the tradeoffs that matter, and then aligning your path forward to your unique goals. Our Diagnostics evolve over time as we identify additional analyses and Systematic Optimizations through our ongoing research and work with clients.

Sample Analysis

See what a deliverable looks like via a blinded detailed 529 analysis here.

The 529 Diagnostic

Our 529 Diagnostic currently contains five primary Systematic Optimizations supported by 12 detailed analyses as shown in the table below. All analyses and recommendations are provided to the client as part of our deliverable.

Table 1: Our 529 Plan Optimization Diagnostic as of October 2025

| Systematic Optimizations | Supporting Analyses |

| 01: Optimize contribution strategy to reach target educational funding needs | – Quantify the expected future cost of college – Model expected % of costs funded by plan based on current value of account(s) and contribution strategy – Calculate revised contribution strategy necessary to reach target funding % |

| 02: Define optimal investment allocation path to funding educational needs | – Define target equity / bond mix by each investment year – Identify which funds to use within the specific 529 plan to implement the investment strategy |

| 03: Optimize 529 tax and funding benefits | – Quantify the incremental tax benefits of using 529 plan to save for college costs – Balance tax benefits with potential costs of being overfunded and other opportunity costs |

| 04: Determine which state’s 529 plan is optimal | – Calculate current plan costs vs. tax benefits – Compare against other state plans to identify opportunities for total cost improvements |

| 05: Develop mitigation strategy to minimize costs of being overfunded (if plan will be overfunded) | – Quantify the incremental costs of being overfunded – Reduce costs through direct mitigation (i.e. Roth Rollover, Beneficiary Updates) – Further reduce costs through tax rate management |

Client Implementation

This Diagnostic is available to our financial planning clients as part of their ongoing deep dives or can be purchased as a standalone, flat-fee project. Email us if you’d like to discuss anything in more detail or learn more about our services.

email: [email protected]

Disclosures:

This content is for educational purposes only and is not an investment recommendation. Employees and clients of Kangpan & Co. may hold positions in securities discussed in this post. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.