2025 Tax Planning Summaries, engineering a Personal Endowment, capital-intensive infrastructure bubbles, and a primer on income-centric investing

Dear Friends and Client Partners,

In this week’s deep dive I’ll be talking a bit about the income strategy I’ve used to create the cashflows that support my family. This portfolio income took the place of my C-level salary when I left the corporate world and also provides the cashflow that allows me to be intentional and measured in who I decide to work with as I build Kangpan & Co.

A number of you have asked about or expressed interest in living off your portfolio as you think about your future so hopefully this is a helpful start. But first, a quick update on Systematic Upgrades we’ve made for our clients’ financial lives.

Systematic Upgrades

Focus: 2025 Tax Planning Summary

We have finalized your 2025 Tax Planning Summaries. These reports highlight actions we took together that have tax implications that are not readily apparent on your W-2s and 1099s (e.g. 529 plan contributions, IRA funding, etc.).

The goal of this summary is twofold: ensuring zero “tax leakage” and reducing the administrative drag on your accounting team. Implementation is as follows:

- Comprehensive Tax Coordination: For clients utilizing our integrated tax coordination services, we’ll be sending summaries directly to you and your CPAs. No action is required.

- Independent Tax Services: For clients managing their own accounting flow, your summary will be securely sent over to you if you have any notable actions.

Deep Dive

Engineering a Personal Endowment

As countless modern philosophers (both academic ones and the armchair variety) have pointed out, two of the hardest addictions to overcome are carbohydrates and a steady paycheck.

The pretzels, frozen waffles, and assorted cookies that we regularly refill at the Kangpan household present no argument against the addictiveness of carbohydrates.

Let’s talk about the monthly salary.

I spent almost two decades in the corporate world, the latter half mostly as a C-level executive. I always had a proclivity for investing and financial planning so I was diligent over the years in contributing a fixed percentage of my salary to my family’s portfolio. This allowed me to “retire” from the corporate world before 40.

However, the strategies that work during accumulation aren’t necessarily the same ones that should be used when switching gears to living off your portfolio.

Low-cost, broad stock indexes with selective exposure to various factors are a great way to build your portfolio while you’re in accumulation mode. These were a core part of my strategy for building my own asset base and they form the foundation for many of Kangpan & Co.’s growth-focused clients.

But predictability, stability, and the preservation of assets are what’s important when you are living off investments.

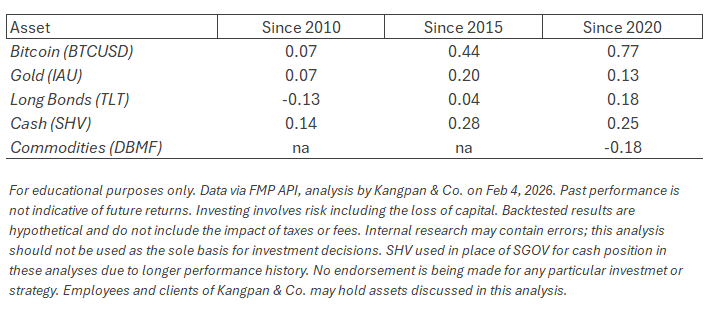

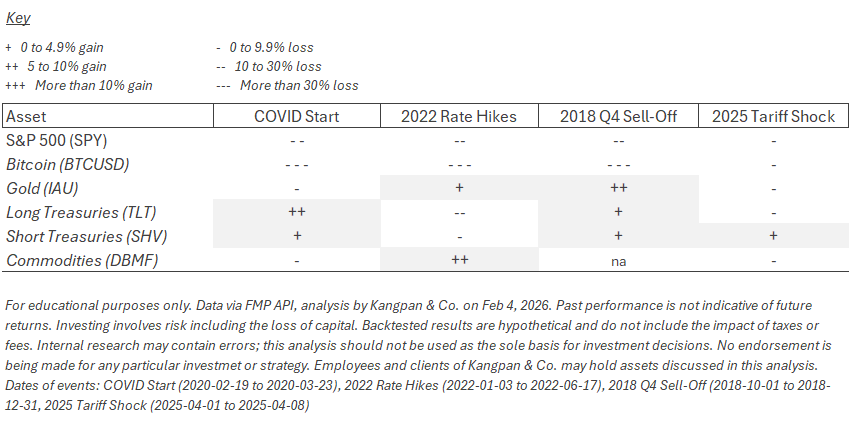

A traditional stock and bond portfolio doesn’t check those boxes as the inflationary 1970s, the 2008 GFC, the synchronized drawdown in 2022, and many other events have repeatedly shown.

These major shock events are incredible opportunities for buying when you have a steady wage to invest into the market. But they create significant sequence of returns risks for anyone living off their investments.

Volatility aside, I also knew I didn’t want a strategy that involved steadily selling the assets I had accumulated. When you spend twenty years or more building up a nest egg via a steady paycheck, it is very difficult to suddenly shift into selling the family jewels to support a post W-2 life.

This means I needed to engineer a portfolio strategy that:

- Generates a predictable income across economic cycles

- Grows that income steadily over time

- Protects the underlying assets against common economic shocks

Essentially, I developed a portfolio strategy that was modeled after how large universities manage their endowments – a Personal Endowment that provided a synthetic, growing income to replace the one I was stepping away from.

This Personal Endowment portfolio is primarily made up of the following strategies:

- Quality-Tilted Equity Income: Companies across a diverse set of industries and geographies that have steadily increasing cashflows, established distributions, and conservative payout and debt ratios.

- Real Assets: Real estate and infrastructure that generate contractual revenue tied to inflation escalators.

- Alternative Credit: Private and senior-secured loans that are primarily floating rate in nature that help smooth the rate sensitivity of the portfolio.

- Economic Hedges: A mix of uncorrelated assets such as managed futures, cash, gold, etc. that help shield the portfolio against major economic shocks. These form the basis of Kangpan & Co.’s Guardian strategy used across many client portfolios.

The exact mix of these assets can vary throughout the economic cycle but I generally aim for a balanced mix of yield and yearly growth of that yield. This allows the portfolio to generate a livable, diversified income today and a steadily increasing cashflow that aims to outpace inflation over time.

So how’s it going?

So far this strategy has done exactly what I wanted it to do.

I designed this Personal Endowment style portfolio because I wanted a stochastic (random) market to support a more deterministic (predictable) life.

It was important to me to be able to comfortably and reliably support my family through our investment portfolio when I left Kepler. This wasn’t because I wanted to retire, but because I wanted to be measured and intentional in how I pursued my second act.

Not needing the income from Kangpan & Co. has allowed me to to focus on working only with clients I enjoy spending time with while supporting them the way I think a full service wealth manager should. I don’t need scramble to build assets and take on clients that aren’t a fit for the firm or compromise Kangpan & Co.’s integrity by accepting commissions for products.

I don’t care about being the biggest wealth manager, I want to be the best for the client partners whom have entrusted their family’s future with my firm. My portfolio strategy gives me the absolute independence from outside pressures to focus on that goal.

If you are interested in looking at the math of supporting a career pivot or retirement with a customized Personal Endowment strategy, let’s sit down and run your specific numbers together.

Food for Thought

A collection of articles or books I’ve read that might be interesting to many of you.

- The AI Debt Boom Does Not Augur Well for Investors via the FT: A reminder that capital-intensive infrastructure booms have historically had permanent, transformative effects on the broader global economy and human behavior…. but can create short to medium term investment pain if the capital cycle turns. As the FT notes:

“History rarely rewards lenders who finance capital-intensive growth booms at their peak. In the late 1990s, telecoms companies borrowed heavily to lay fibre-optic cables, confident that data demand would ensure adequate returns. Although the infrastructure transformed the economy, it generated little return on investment for years.”

- The Ultimate Dividend Playbook by Josh Peters: For anyone interested in learning more about income-centric investing (a least in terms of equities). This is a solid primer on assessing the quality and sustainability of payments from publicly traded firms. The appendix also provides a great series of briefings on investing in various industries like utilities, REITs, and more. I don’t agree with all the valuation methods but the book provides a strong foundation from which to expand.

Thank you for the continued partnership and for the opportunity to help steer your family’s capital toward what matters most.

Nathan

Founder & Lead Advisor

Not a client yet?

Subscribe to this bi-monthly client update for free to see all the engineered tax, investing, and planning strategies we run for high-earning and high net worth investors like you.

Or reach out to us to get a complimentary, 30-minute Diagnostic to see what tax, investing, and planning opportunities your current strategy or advisor is overlooking.

Disclosures: This content is for educational purposes only and is not investment, tax, or legal advice. No post is an endorsement of any particular strategy or security. The Personal Endowment is a conceptual investment framework customized to each client and does not represent a specific fund or guaranteed outcome. Asset allocation and yield targets are subject to market volatility. We do not receive any direct payments or commissions for securities discussed in our posts. Employees and clients of Kangpan & Co. may hold positions in securities discussed in posts. Speak with a licensed tax, legal, or financial advisor before making any changes to your investments or financial strategies. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.