If you’re trying to live off portfolio income, you need to bring together stable, after-tax income from diversified sources. And very few asset classes look better on paper for this purpose than mature, cash-flowing real estate properties.

I’ve always wanted to own a broadly diversified real estate portfolio for the predictable, monthly income. But, as Sheila can attest to, my handyman skills don’t extend much beyond putting together Ikea furniture and hanging the paintings we find antiquing.

Enter Private Real Estate Funds.

In this primer we’ll cover:

- What is a Private Real Estate Fund?

- The three key benefits they can bring to a portfolio

- The downsides of this asset class

What is a Private Real Estate fund?

As the name implies, Private Real Estate funds are investment vehicles that primarily invest in… real estate. This could be any type of real estate from multi-family housing to data centers.

Since the underlying assets are physical properties charging rent, returns from these funds typically include a meaningful dividend yield as well as underlying appreciation of the assets over time.

These funds are typically managed by an outside investor who charges a fee for sourcing and managing the underlying investments. Private funds are not traded on stock exchanges but can be purchased through certain financial advisors. The partnerships we’ve developed ensure clients of Kangpan & Co. have access to many of the same institutional funds that the private investment arms of large banks do.

Before we dig into the characteristics that make Private Real Estate funds a core component of the Personal Endowment investment portfolio, I need to note that these funds are generally for accredited investors as defined by the SEC. This post is for educational purposes only and is not an investment recommendation or endorsement of anything specific strategy or fund. Kangpan & Co. is a fee-only RIA, we do not accept commissions or any other form of compensation from fund providers. We like our recommendations to clients to be free from conflicts of interest.

Now let’s get to three ways these funds can benefit a portfolio.

Benefit 1: Diversification vs. Other Core Assets

If you’re trying to build a portfolio that generates income across different types of economic environments, you need genuine diversification. Investments need to have returns with low long-term correlations to each other so that when a shock hits, your entire portfolio doesn’t move in the same direction at once.

This is the canonical argument for holding both stocks and bonds. But as 2022 demonstrated clearly, a two-asset portfolio has real limits. When inflation drove interest rates sharply higher, both stocks and bonds fell simultaneously, leaving portfolios that assumed low correlation between the two with nowhere to hide.

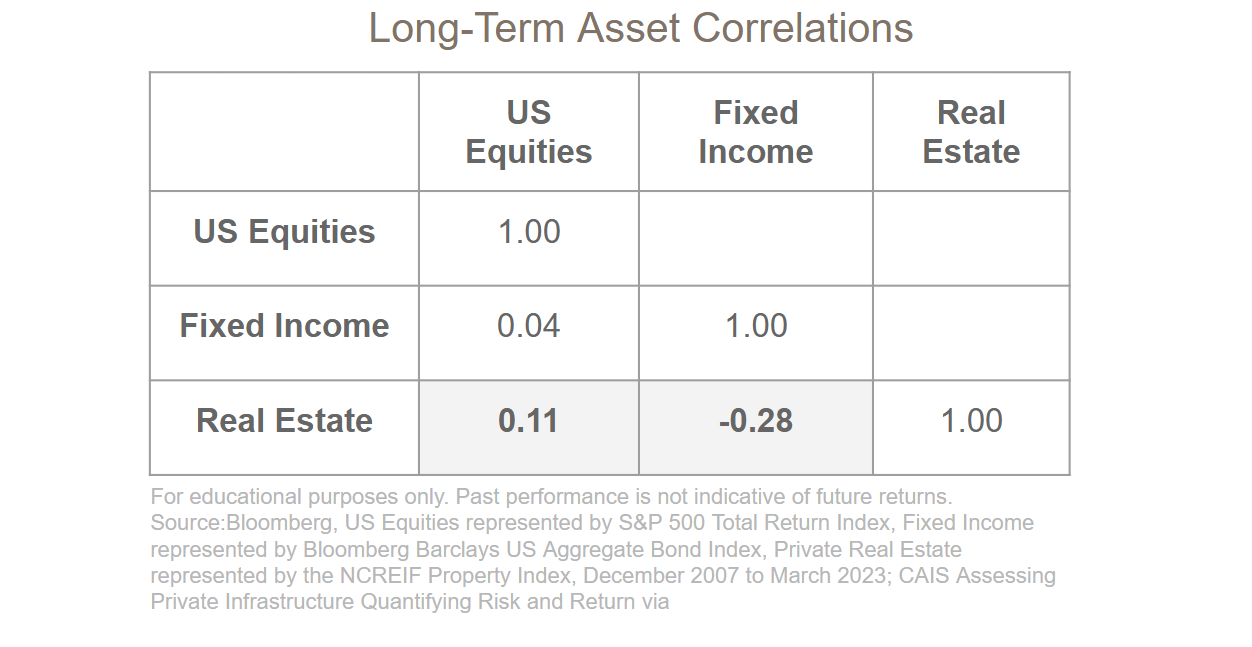

Private real estate has historically shown low correlation to both public equities and fixed income. According to an analysis from CAIS, private real estate returns have had a correlation of approximately 0.11 to the S&P 500 and -0.28 to the Bloomberg Aggregate Bond Index over a recent 15-year period.

The economic drivers of real estate returns – rental income, occupancy rates, property values – respond to different forces than corporate earnings or interest rate movements, even if they’re not entirely immune to macro conditions.

This doesn’t mean private real estate is uncorrelated to everything all the time. A severe recession can affect private real estate too. But adding it to a portfolio of dividend equities and fixed income creates a third set of return drivers (which is the point).

Our Personal Endowment portfolios incorporate real estate positions by default as well as additional asset classes to further diversify income sources.

Benefit 2: Tax-Deferred Income

Much like an individual investing directly in an apartment building, certain non-cash expenses like depreciation are deducted from the income generated by properties owned by private real estate funds.

These deductions get wrapped into what’s known as Return of Capital, or ROC. ROC distributions aren’t taxed as current income. Instead they reduce the cost basis of your investment over time, deferring the tax liability until you eventually sell. Potentially at lower long-term capital gains rates rather than ordinary income rates.

For someone living off portfolio income, or for anyone in a meaningful tax bracket, this distinction is significant.

Here’s how this works in practice.

Let’s say you’re in the 35% federal tax bracket and pay state taxes of 5.0%. We’ll ignore NIIT and local taxes for now to keep things simple.

Scenario 1: You have $300k in a taxable corporate bond fund that yields 4.5%.

- $300k * 4.5% yield = $13,500 in pre-tax income

- $13,500 * 40% combined tax rate = ~$5,400 in taxes

- Leaving you with $8,100 after-tax income

Scenario 2: Let’s look at the same math with a Private Real Estate fund that also yields 4.5% but 80% of it categorized as ROC.

- $300k * 4.5% yield = $13,500 in pre-tax income

- $13,500 * (1-80% ROC) = $2,700 in taxable income

- $2,700 taxable income * 40% tax rate = $1,080 in taxes

- Leaving you with $12,420 after-tax income

Same yield. Same tax bracket. $4,320 more in your pocket annually simply from how the income is classified. On $300,000 that’s a 53% improvement in after-tax income from a single asset class.

Keep in mind, this example was only looking at the yield of a private real estate fund and not underlying appreciation of the fund’s properties which can add even more to the total return over time.

ROC can range significantly between funds and shouldn’t be the primary lever you look for when evaluating options. That said, we always look at ROC for funds within our Personal Endowment portfolios since we use these strategies to optimize after-tax income for our clients.

If you’re wondering how much of your current portfolio income is being unnecessarily eroded by taxes, this is one of the first things we look at in our Personal Endowment review. Contact us or schedule a complimentary consultation if you want us to audit your current situation.

Benefit 3: Reduced Volatility via Appraisal-Based Pricing

Public stocks and bonds are priced continuously by the market. Every piece of news, every Fed statement, every earnings miss moves the price in real time – often dramatically and in ways disconnected from the underlying business fundamentals.

Private real estate funds are generally valued quarterly through formal appraisals by standardized internal pricing models and independent valuators. The inputs are things like rental income, occupancy rates, cap rates, and comparable property transactions – not sentiment, momentum, or a Twitter thread about interest rates.

What this means practically is that the reported value of your private real estate allocation moves more slowly and in response to genuine changes in the underlying properties. This has the effect of dampening the day to day swings in your portfolio.

It’s important to clarify, appraisal-based pricing doesn’t mean you’re getting a better deal than the market would offer. It just means the price reflects a fundamental assessment of the asset rather than a real-time market clearing price. The valuation of a private real estate fund could be lower or higher than publicly traded REIT equivalents depending on current market sentiment.

What are the risks of Private Real Estate Funds?

No asset class is without tradeoffs, and private real estate funds have specific ones worth understanding clearly before investing.

Gated redemptions: Unlike a stock or ETF you can sell tomorrow, private real estate funds typically have strict limits on when and how much you can redeem. Most funds allow redemption on a quarterly basis with meaningful advance notice requirements, and during periods of market stress funds can gate redemptions entirely. Meaning you cannot access all your original capital regardless of how much you need it in the moment. This is the illiquidity premium at work. You earn higher after-tax income in part because you’re accepting that the capital is not freely accessible. For anyone investing in these funds the capital should be genuinely long-term, money you don’t need to touch for five to seven years minimum.

Manager Quality and Fees: In a public index fund the manager is largely irrelevant — you’re buying the market. In private real estate, the manager’s skill at sourcing deals, managing properties, and timing the cycle determines a significant portion of your return. And the managers get paid to do this work. Private fund fees can be meaningful, typically 1% to 1.5% in management fees plus performance incentives. Private funds need to be evaluated against the net return of fees they deliver rather than the topline gross return marketing materials may highlight. We evaluate our funds carefully before recommending them and access institutional share classes where available to minimize fee drag.

Valuation Opacity: Quarterly appraisals reduce volatility but also mean you have limited visibility into what your investment would actually fetch in a sale at any given moment. The reported value of a private real estate fund should be treated as an estimate rather than a market price. Some funds report when they sell their underlying assets and comparing the market price they receive for their assets vs. the underlying valuation can be a good way to check the fund’s homework.

The Bottom Line

Private real estate funds are not right for every client or every dollar. They require genuine long-term capital, tolerance for illiquidity, and access to institutional-quality managers. Which is why they remain largely unavailable to retail investors outside of advisor relationships.

For accredited clients that want portfolio diversification and tax-deferred income streams, we feel private real estate funds earn their place. This is particularly the case for accredited investors that want to build a Personal Endowment style portfolio – the tax efficiency, the income stability, and the diversification against public market volatility all serve the core goal: durable, growing income that doesn’t require selling principal.

If you’re building towards a life fueled by portfolio income and want to understand how private real estate fits into your specific situation, contact us or book a complimentary consultation.

Not ready to talk yet? Every letter in this series goes deeper into how the Personal Endowment works – subscribe to get them directly.

Food for Thought

- The Historical Benefits of US Private Real Estate via Invesco: A deeper look at how US Private Real Estate as an overall asset class has performed over time vs. stock and bonds

- Is it Better to Rent or Buy via The Economist: Buying a home doesn’t always come out ahead financially vs. renting long term. It all depends on interest rates, rent levels, etc. At the end of the day, even if the math doesn’t work out, owning the home you raise your family in has emotional benefits that far outweigh what the numbers say either way.

Thank you for being part of our community – whether you’re a client, a reader, or somewhere in between. If this letter resonated with your own situation, I’d genuinely enjoy hearing about it.

Nathan

Founder & Lead Advisor

Disclosures: This content is for educational purposes only and is not investment, tax, or legal advice. No post is an endorsement of any particular strategy or security. We do not receive any direct payments or commissions for securities discussed in our posts. Private funds are generally available only to ‘Accredited Investors’ as defined by the SEC. The Personal Endowment is a conceptual investment framework customized to each client and does not represent a specific fund or guaranteed outcome. Employees and clients of Kangpan & Co. may hold positions in securities discussed in posts. Speak with a licensed tax, legal, or financial advisor before making any changes to your investments or financial strategies. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.