This is a collection of our insights, research, and strategies that we publish here to highlight how we think about the world. Subscribe to our newsletter for a more curated, weekly update.

This post is a brief primer on Playbooks, our unique approach to systematically delivering comprehensive analyses and recommendations for our clients.

Given my engineering and technology background, we build most of our services and strategies on a modular basis via individual Systematic Optimizations. This allows us to become experts at optimizing the individual components of a client’s investment and financial strategy through a continuously evolving, methodical process. Our library of Systematic Optimizations grows alongside our firm over time so our clients will be able to experience compounding improvements to their financial lives with each year they work with us.

A Playbook is a structured way to navigate and prioritize these optimizations based on a client’s goals or needs. Each Playbook is a curation of these individual optimization aligned to a specific theme (i.e. Portfolio Tax and Fee Efficiency Optimization) or to a particular client’s needs based on their customized financial plan.

These Playbooks, and the individual optimizations within each, are shared openly and transparently with our clients so they are always aware of what analyses we are doing, how we’ve arrived at our recommendations, and the impact we are having on their financial journey. The Playbooks also provide a clear prioritization for next steps for our advisors and their clients between meetings and help us track the cumulative improvements and optimizations we have made together.

All Playbooks are available to our financial planning clients as part of their ongoing deep dives or can be purchased as a standalone, flat-fee project. Email us if you’d like to discuss anything in more detail or learn more about our Playbook-based approach to delivering continuously improving financial outcomes.

Disclosures: This content is for educational purposes only and is not an investment recommendation. Employees and clients of Kangpan & Co. may hold positions in securities discussed in this post. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.

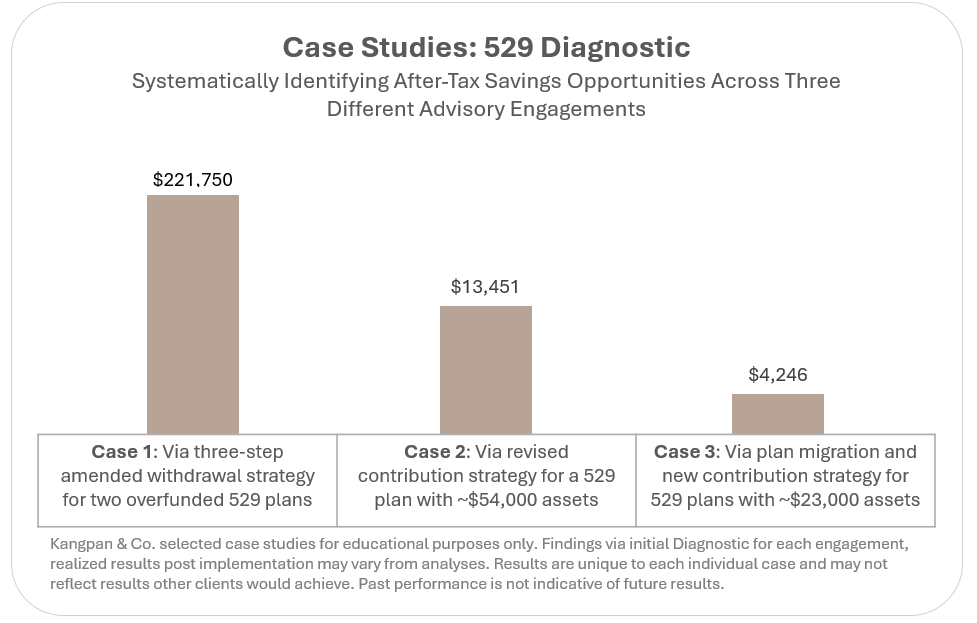

This post details our approach to optimizing a client’s college savings strategy using a Diagnostic. Check out our primer posts on Systematic Optimization and Diagnostics to learn more about our unique approach to financial advisory .

It’s common to wonder whether you’re saving enough for your children’s educational needs and to also be unsure what the tradeoffs are to being underfunded vs. overfunded. Our 529 Plan Diagnostic is designed to quickly give clear answers to these and other common questions while enabling us to provide a comprehensive, tailored recommendation for improving your overall approach to college savings.

As with all our Diagnostics, this structured approach ensures we are comprehensively examining your situation in a methodical way, quantifying the tradeoffs that matter, and then aligning your path forward to your unique goals. Our Diagnostics evolve over time as we identify additional analyses and Systematic Optimizations through our ongoing research and work with clients.

Our 529 Diagnostic currently contains five primary Systematic Optimizations supported by 12 detailed analyses as shown in the table below. All analyses and recommendations are provided to the client as part of our deliverable.

Table 1: Our 529 Plan Optimization Diagnostic as of October 2025

Systematic Optimizations

Supporting Analyses

01: Optimize contribution strategy to reach target educational funding needs

– Quantify the expected future cost of college – Model expected % of costs funded by plan based on current value of account(s) and contribution strategy – Calculate revised contribution strategy necessary to reach target funding %

02: Define optimal investment allocation path to funding educational needs

– Define target equity / bond mix by each investment year – Identify which funds to use within the specific 529 plan to implement the investment strategy

03: Optimize 529 tax and funding benefits

– Quantify the incremental tax benefits of using 529 plan to save for college costs – Balance tax benefits with potential costs of being overfunded and other opportunity costs

04: Determine which state’s 529 plan is optimal

– Calculate current plan costs vs. tax benefits – Compare against other state plans to identify opportunities for total cost improvements

05: Develop mitigation strategy to minimize costs of being overfunded (if plan will be overfunded)

– Quantify the incremental costs of being overfunded – Reduce costs through direct mitigation (i.e. Roth Rollover, Beneficiary Updates) – Further reduce costs through tax rate management

Client Implementation

This Diagnostic is available to our financial planning clients as part of their ongoing deep dives or can be purchased as a standalone, flat-fee project. Email us if you’d like to discuss anything in more detail or learn more about our services.

Disclosures: This content is for educational purposes only and is not an investment recommendation. Employees and clients of Kangpan & Co. may hold positions in securities discussed in this post. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.

This post provides more detail on how we develop a Core portfolio strategy for our clients. This post should also help potential clients better understand how our mindset and approach may be different from the typical advisor.

The Role of the Core Portfolio

Designing and managing a Core portfolio is one of the foundational investment management services we provide to clients. As the name implies, the Core portfolio should be the reliable engine to take an investor from where they are today to where they want to be in the future with as minimal drama as possible. The Core portfolio is where an investor will keep the majority of their assets. This means a Core portfolio must adhere to our three key investing tenets:

Short term returns for any asset class are unpredictable so a Core portfolio needs to be truly and widely diversified across uncorrelated asset classes

Base rates are a strong guide to long-term returns so we should make decisions on which assets to include and in what proportions based on robust historical data that covers a wide range of business and economic cycles; these assets will be held for the long term and rebalanced to target allocations rather than actively traded

Avoid permanent losses of capital in this portfolio by focusing on funds of diversified assets and strategies with established, audited track records rather than becoming overly concentrated in individual stocks or securities; we will be methodical in how we administer the portfolio such as minimizing tax drags based on where we locate assets, rebalancing the portfolio, and selecting funds to be included

The Core portfolio is primarily composed of a customized mix of low-cost, diversified ETFs across the following asset categories:

Equities (Stocks): These are the primary drivers of long-term returns within most portfolios. Depending on a client’s comfort with risks and return objectives, we integrate a mix of equities that span different geographies (i.e. US, International) and different factors (i.e. Large Cap Growth, Small Cap Value)

Fixed Income (Bonds): These can be used to provide steady income within a portfolio or function as ballast for when equities experience stress periods. Depending on a client’s income needs and risk tolerance we will look to include fixed income options that span a range of durations and credit qualities.

Alternatives: These are investments we use to further diversify the mix of Stocks and Bonds in a portfolio ideally seeking to increase returns while reducing overall risks. Assets used here could include commodities such as gold, managed futures, structured credit, etc.

Our comfort with alternative investments is one of the traits that makes us different from typical advisors. For examples on how we think about how alternatives can improve the return / risk profile of a portfolio, check out our post about gold’s role in portfolio or our post about how structured credit like AAA CLOs can enhance yields.

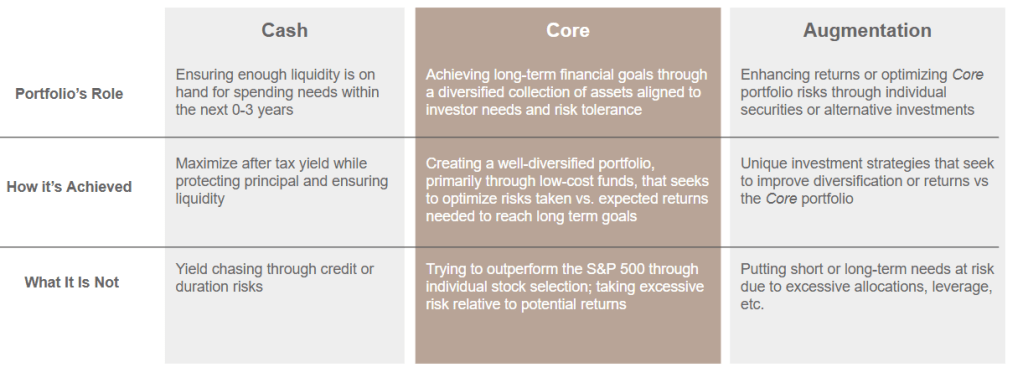

While the Core portfolio generally does the bulk of the heavy lifting for an investor, it’s important to point out that we feel investors should have two other types of portfolios to form a well-rounded investment plan: a Cash portfolio and an Augmentation portfolio. The table below highlights key aspects of each portfolio and we will discuss the other two portfolios in more depth in future posts.

Building a Client’s Core Portfolio

While there are common building blocks across the Core portfolios we manage, we customize each one to the unique needs and risk tolerances of every client. This is typically done by following three key steps.

Step I: Understand a client’s goals and timeframes to establish a target return

In order to determine what return we need from our portfolio, we first need to figure out where we are at and where we are trying to go. Many investors have a vague sense of wanting to “retire earlier” or “build more wealth,” but we need to better quantify those notions in order to create objective targets. Once we know our goals, we can then figure out what return we need from our portfolio. This is something we work closely with our clients to understand before we make any investments.

Let’s go through an example to help illustrate what we’re talking about.

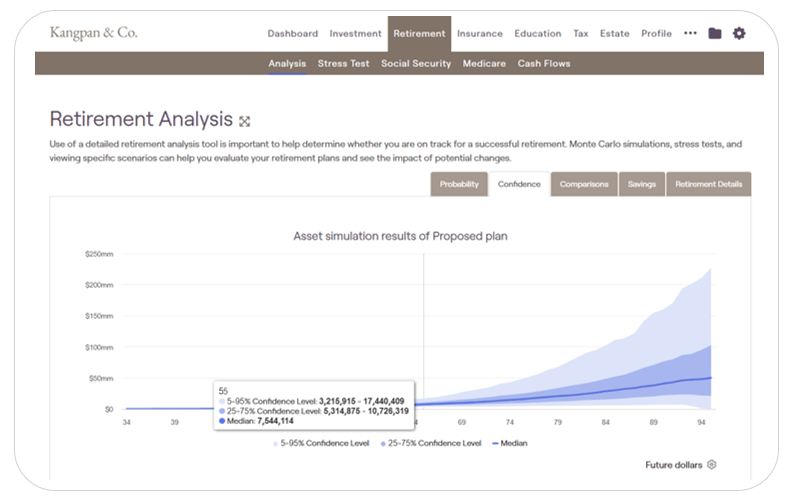

The Johnson’s are a family of two working professionals in their mid 40’s with two kids. They currently have an investable portfolio of $1.8 million and want to retire in 10 years with $7.5 million. They expect to be able to add $200,000 a year to their investable assets between now and then.

Using our dynamic planning tools, we determine together that they will need to earn a return of at least 8.9% a year over the next 10 years to reach their $7.5 million goal.

Illustrative example using Kangpan & Co. planning tools to determine expected asset levels along with associated confidence intervals. Modified for demonstration purposes.

Step 2: Understand a client’s comfort with risk and return to establish a baseline allocation using traditional assets (i.e. Stock and Bond mix)

The baseline rate of return of a Core portfolio is predominantly determined by its ratio of Stocks to Bonds. This forms the baseline allocation of the portfolio. Alternatives, which we discuss in the next step, are used to manage the risk profile of a portfolio.

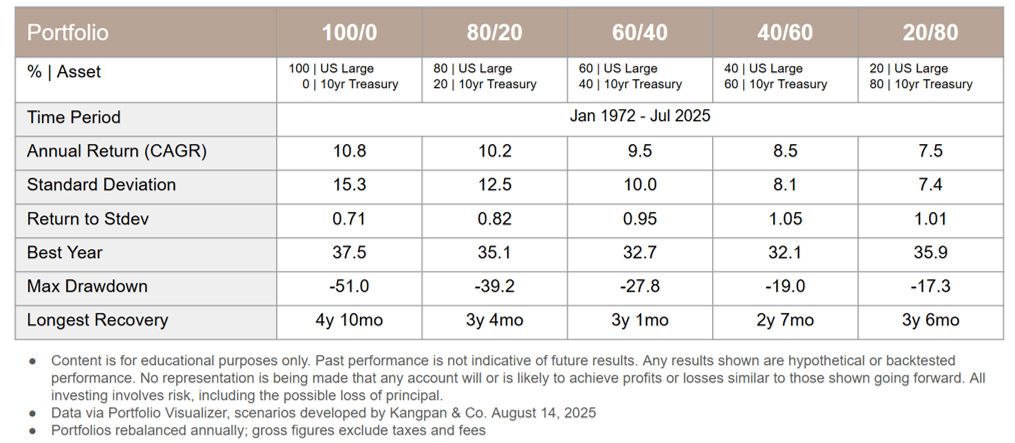

The table below shows the long-term historical performance and key risk metrics of various mixes of Stocks/Bonds that we pulled together using Portfolio Visualizer’s asset backtesting module. We show tables like this to clients to guide conversations about what baseline mix should be used as a starting point to reach their return goals.

Each column represents the results for a different mix of Stocks/Bonds with Stocks represented by US Large Caps (a proxy for the S&P 500) and Bonds represented by 10yr Treasuries. For example, the column 100/0 is a portfolio comprised of 100% Stocks and 0% Bonds while the 60/40 column is a portfolio of 60% Stocks and 40% Bonds.

We can see based on the table that in order for the Johnson family to get their target 8.9% return, they will need to have a portfolio that is somewhere between a 40/60 portfolio (with an 8.5% expected return) and a 60/40 portfolio (with a 9.5% expected return).

Table 1: Return and Risk Profiles for Various Stock/Bond Portfolio Mixes

However, in addition to understanding how returns are affected by the mix of Stocks and Bonds in a portfolio, we also use the data in this table to better understand how our clients feel about risk. Specifically we look at data points like how volatile the portfolio is on a year to year basis, how severe downturns have been (the Max Drawdown metric), and how long each portfolio took to recover from those downturns.

Step 3: Adjust the return and risk profile of the baseline portfolio to the client’s needs by more broadly diversifying the base asset mix and selectively incorporating alternatives

Our first step identified what minimum return level we need to target in order to help our client reach their goals on the timeline they desire. Our second step gave us a better understanding of how the client views the tradeoffs between risks and potentially higher returns. These prior two steps give us the inputs we need for our final step with a client… fine-tuning the risk and reward ratios of a baseline Stock and Bond portfolio by introducing additional diversifiers.

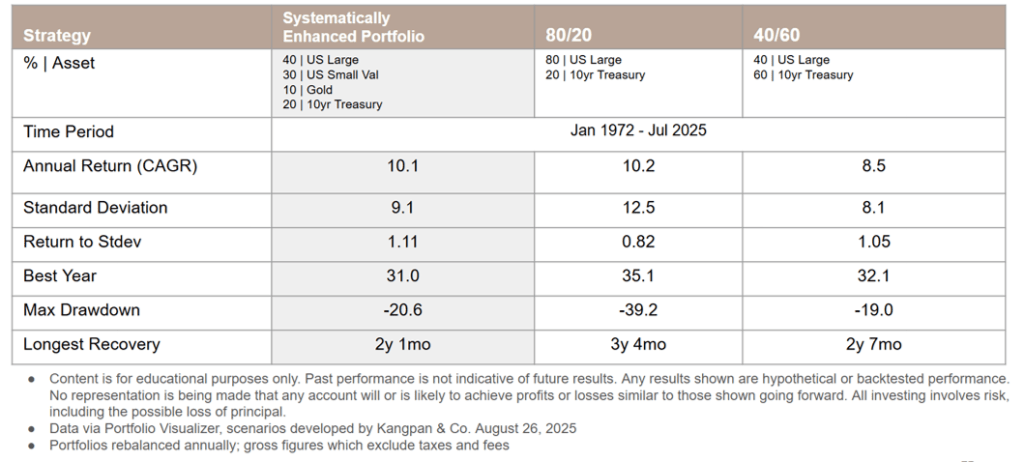

Let’s say in our discussion with the Johnson’s in the prior step that they liked the idea of retiring with $8.3 million instead of $7.5 million if they could earn the historical 10.2% returns of an 80/20 portfolio (who wouldn’t?). However, among other issues, they did not like the amount of additional risk that came with that portfolio’s Max Drawdown of -39.2% vs. the 40/60 portfolio’s -19.0%.

This is where we can use a wider range of funds and alternative assets to help our clients balance the returns they want with the potential risks of a portfolio. In the table below, we are showing a simplified example of enhancing the portfolio with just two additional asset classes:

US Small Cap Value: research shows US Small Caps and Value factors tend to outperform US Large Caps over time

Gold: an alternative asset class that can help diversify portfolios consisting of Stocks and Bonds

Strategically incorporating these two additional asset classes allows us to boost backtested returns to the levels of an 80/20 portfolio while having the risk characteristics more aligned to a 40/60 portfolio:

Table 2: Returns and Risks for Systematically Enhanced Portfolio vs. Stock / Bond Mixes

This is where the power of being open to incorporating alternatives comes into play for clients – we can better engineer a portfolio’s returns and risks to meet the unique needs and desires of each client.

We primarily use alternatives in publicly available ETFs rather than private options because they are generally:

More transparent: so both our advisors and our clients are clear on what is being added to the portfolio

More liquid: the tradability of ETFs makes rebalancing or strategic shifts in allocations much easier to accomplish

Lower fee: ETFs tend to (but not always) have lower fees than private funds for similar strategies and implementations

Real-World Client Implementation

The example in the prior section is purely illustrative and for educational purposes only. In the real world, we look across a much broader set of investable options across stocks, bonds, and alternatives. The actual individual securities and funds we use to set up our clients’ positions which will have a different return and risk profile from those based on overall asset class returns used in our example.

Our clients benefit from the ongoing research we conduct for each asset class inlcuding:

How the asset class relates to the rest of the portfolio by understanding historical correlations, stress periods, return and risk profile, etc.

How different allocation weights affect the overall portfolio’s risk and return metrics across various time periods

Our preferred fund or individual security(ies) for gaining access to that asset class

Our selection process for specific securities we use in portfolios depends on the asset class we are researching and our clients’ specific needs. For examples of some of the factors we consider check out our post on selecting an ETF for S&P 500 exposure or our preferred International funds

Once a Core portfolio strategy has been developed, we then help clients implement and manage the portfolio on an ongoing basis including:

Reporting / Monitoring

Rebalancing

Tax-Loss Harvesting

Adding / Removing Assets Over Time

Our fees and minimums for designing and managing a Core portfolio strategy can be found in the Service Models & Pricing section of our investing services page. We also work with clients on a flat-fee project basis for those that just want access to our portfolio advice and construction process rather than ongoing management.

Email us if you’d like to discuss anything in more detail or learn more about our services.

Disclosures: This content is for educational purposes only and is not an investment recommendation. Employees and clients of Kangpan & Co. may hold positions in securities discussed in this post. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.

This post examines how incorporating gold into a portfolio of US stocks and bonds can improve overall returns as well as lowering overall volatility. We typically use the analyses shown here, in combination with other data points, to guide conversations with clients about including a gold allocation within their Core portfolios.

There are numerous reasons investors incorporate gold into their portfolio, but ours come down to the following key points:

Gold exhibits very low correlation to stocks and bonds of 0.00 to 0.09 since the 1970s, making it a powerful diversifier to a portfolio primarily made up of those assets1

Gold is predominantly priced in US dollars across global markets making it a particularly good hedge position for US-based investors2

Gold’s long-term return measured in US dollars from 1971 (after being de-linked from the dollar) to 2023 is 8% outpacing US inflation and various US Treasuries3

We are also well aware of the arguments against holding gold, but we prefer to focus on what real world data says, not on theoretical criticisms. One of the traits that makes us different from other advisors is our focus on empirical evidence and our willingness to do our own homework.

We’ll explore each of the points in favor of gold in more detail in future posts. For today, we’re going to spend the rest of this article highlighting the historical impact gold has had on a stock and bond portfolio’s returns and risk metrics.

Portfolio Analysis

We used Portfolio Visualizer’s “Backtest Asset Allocation” module to develop the analyses shown in the table below. We’ll look at three scenarios to understand how adding gold affects the return and risk characteristics of a 60/40 portfolio. In each scenario below, the ratio of Stocks to Bonds stays at a consistent 60/40 ratio to each other with Gold representing 0%, 5%, and then 10% of the total portfolio mix.

Table 1: How Gold Impacts a 60/40 Portfolio – Jan 1972 through Aug 2025

60% Stocks 40% Bonds 0% Gold

57% Stocks 38% Bonds 5% Gold

54% Stocks 36% Bonds 10% Gold

Topline Metrics

Annual Return (CAGR)

9.48%

9.60%

9.70%

Annual Stdev

10.11%

9.70%

9.41%

Return/Stdev

0.93

0.99

1.03

Max Drawdown

-28.5%

-24.5%

-22.5%

Stress Periods

Dotcom Crash

-18.4%

-16.8%

-15.2%

Subprime Crisis

-26.4%

-24.5%

-22.5%

COVID Shock

-9.6%

-9.1%

-8.7%

For educational purposes only. Data and analytics via Portfolio Visualizer run on September 29, 2025. Scenarios developed and summarized by Kangpan & Co. Assumes yearly rebalancing and does not include the impact of fees or taxes. Stocks are represented by “US Stock Market,” Bonds represented by “10-year Treasury,” and Gold represented by “Gold.” Stress Periods: Dotcom Crash Mar 2000 – Oct 2022, Subprime Crisis Nov 2007 – Mar 2009, COVID Shock Jan 2020 – Mar 2020. Past performance is not indicative of future returns. Investing involves risk including the loss of capital.

There are two key takeaways from the chart that we want to highlight for readers:

Increasing allocations to Gold result in increasing Annual Returns along with decreasing volatility (as measured by the Annual Standard Deviation) thus improving the overall Return/Stdev ratio

Incorporating Gold makes the portfolio more resistant to shocks and stress, lowering the observed overall Max Drawdown of the portfolio and reducing the losses experienced across numerous Stress Periods

Overall, the data and analysis shows adding gold to a standard portfolio of stocks and bonds tends to increase expected annual returns while decreasing its risk profile.

Implications for Investor Portfolios

We feel the table above is a compelling set of data points to argue in favor of including gold allocations within traditional stock and bond portfolios. When we work with clients who have an interest in diversifying their portfolio with gold, we will also help them:

Identify the optimal starting allocation based on the rest of their portfolio and their overall risk tolerance

Determine how to incorporate gold into their portfolio such as utilizing an ETF vs. holding physical gold

Manage the additional complexity of including more assets within their portfolio such as rebalancing, broader tax-loss harvesting, etc.

Email us if you’d like to discuss anything in more detail or learn more about our services.

This is going to be a short one. I’m surprised how often I come across individual investors who hold State Street’s SPDR S&P 500 ETF Trust (ticker: SPY) over Vanguard’s S&P 500 ETF (ticker: VOO). What’s the difference between these two? Not a lot besides fees, at least for the typical medium to long-term investor1.

As of the date of this post, SPY has an expense ratio of 0.0945% while VOO sits at 0.03%. That means for every $1,000,000 invested in SPY, you are paying $945 a year in fees to iShares. The same amount invested in VOO translates to $300 a year going to Vanguard. This is a $645 a year difference for two very similar products that track the same index.

Paying the lowest fee for a fund isn’t necessarily the best strategy to pursue when you are looking across different types of strategies. An alternative credit ETF has a different operational setup and risk / return profile than a large cap index ETF. But fees are very important when comparing funds that track the same strategy and index.

If all things are more or less equal between two ETFs, then the lower fee version should have consistently higher returns roughly equal to the gap in fees. Let’s take a look at the average annual performance for SPY vs. VOO to see if the lower fees on VOO appear to translate to higher returns:

Ticker

YTD

1yr

3yr

5yr

10yr

SPY

10.71%

15.85%

19.40%

14.64%

14.46%

VOO

10.79%

15.96%

19.53%

14.70%

14.57%

Market price returns are before tax and inclusive of reinvested dividends and net of fund fees as of August 31, 2025. Data from each provider’s website.

What you see is a pretty consistent 0.06% to 0.13% performance lag from SPY vs. VOO across all time periods above. Other factors can affect performance such as tracking error as well as premiums / discounts to NAV but we believe the fee difference is a significant contributor to the performance difference in this case.

This is an example where knowing what to do (invest in a low-cost S&P 500 ETF) is not the same thing as knowing how to do it optimally. We focus a lot on the optimal here at Kangpan & Co. since we believe even seemingly small Systematic Enhancements can compound into significant benefits to our clients over time. In this case, it’s not just the $645 a year for every $1,000,000 a client has invested in a S&P 500 tracker. It’s the tens of thousands of dollars that translates into when you consider a) that fee difference is lost to the investor every year and b) those fees lost out on reinvested compounding returns.

As a reminder, we do not accept commissions or other forms of direct compensation from any third parties. This post is our own unbiased research and analysis.

Email us if you’d like to discuss anything in more detail or learn more about our services.

Disclosures: This content is for educational purposes only and is not an investment recommendation. Employees and clients of Kangpan & Co. may hold positions in securities discussed in this post. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.

1. There are other considerations such as differences in liquidity, premium / discount to NAV, etc. that could impact some types of investors such as very active traders

I spent nearly two decades leading engineering and analytics teams before becoming a financial advisor. This shaped how I think about financial planning and investing in significant ways. One of those is the power of Systematic Optimization. Seemingly small improvements to individual components can have substantial impacts on an overall system when performed continuously over time.

This led me to developing our Systematic Optimization philosophy and approach to working with clients. This is a structured method of consistently identifying and applying individual optimizations and improvements so that the result of these enhancements over time is far greater than the sum of the individual parts.

Depending on the size of a client’s portfolio, each of our optimizations could save anywhere from a hundred dollars a year to thousands of dollars a quarter. But it’s not the size of any individual optimization that matters, it’s the combination of:

The compounding impact of these optimizations over time

The sheer volume of optimizations we methodically make with clients as we work with them which we estimate could easily number into the hundreds of individual adjustments

The Compounding Impact of Small Changes

Finding an opportunity to save an extra $100 today through a financial optimization is a nice, small win. It’s about the cost of a mid-week meal out with the family at the local pizza shop. But the real power comes when you take into consideration:

Repeating Effects: If that $100 optimization is a yearly, recurring benefit then it’s not just the $100 you saved today but a benefit you’ll realize every year going forward. Tallied up over 40 years, that simple optimization today will save you at least $4,000.

Compounding Effects: If you reinvest that yearly $100 at an 8.0% return, then the cumulative sum of that recurring $100 every year compounding over 40 years is $27,978.

Table 1: Value of $100 Compounded at 8.0% For X Years

Years

Value

Years

Value

1

$108

21

$503

2

$117

22

$544

3

$126

23

$587

4

$136

24

$634

5

$147

25

$685

6

$159

26

$740

7

$171

27

$799

8

$185

28

$863

9

$200

29

$932

10

$216

30

$1,006

11

$233

31

$1,087

12

$252

32

$1,174

13

$272

33

$1,268

14

$294

34

$1,369

15

$317

35

$1,479

16

$343

36

$1,597

17

$370

37

$1,725

18

$400

38

$1,863

19

$432

39

$2,012

20

$466

40

$2,172

The recurring and compounding effect of saving just $100 a year is why we care about making Systematic Optimizations to our clients’ financial lives. Of course, $100 a year is a fairly small improvement, imagine the impact that an optimization resulting in thousands of dollars a quarter could have for a HNW household.

These aren’t part of some black-box codex to which only we the keys. In fact, we write openly and frequently about these optimizations to help educate the broader investor universe and show clients how we approach them.

The value we deliver to clients is often the sheer volume (the hundreds of optimizations that we do over time) and methodical implementation (making sure they are done correctly) of these improvements.

Email us if you’d like to discuss anything in more detail or learn more about applying Systematic Optimization to your own financial affairs.

Disclosures: This content is for educational purposes only and is not an investment recommendation. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.

This post provides an introductory overview of how optimizing Asset Location can help investors reduce tax drags on their overall portfolio. We provide a simplified example to illustrate how a hypothetical high-earning couple in California with ~$1.7m in investable assets could save $6,370 in taxes through a more tax-efficient asset allocation between their taxable and tax-advantaged accounts.

Here are the assumptions for this example:

John and Jane are a high-earning couple in their late-30s working and living in California

They have a combined income this year of $832,000 putting them in the 37% Federal and 10.30% CA state tax brackets (assuming they will file Married, Filing Jointly). We’ll hold off on local taxes for this example.

The couple have $790,000 spread across various Traditional IRA and 401k accounts and $915,000 in taxable investment accounts

John and Jane know the basics of personal finance and hold a diversified 60/40 stock and bond allocation within each of their investment accounts (i.e. they have a 60/40 split in their 401k plans, a 60/40 split in their brokerage investments, etc.)

We’re going to spend the rest of this post examining how shifting assets across John and Jane’s various portfolios will help them reduce their overall tax drag. Instead of using a 60/40 allocation within each investment account they have against, we will look at all their investments in aggregate in order to determine a more tax-efficient strategy across their accounts.

To simplify this analysis we will:

Focus just on the impact of taxes on the dividends or distributions from investments

Treat all qualified accounts as one portfolio which we’ll called Tax-Advantaged Accounts and all taxable accounts as another portfolio which we’ll call Taxable Accounts

Use a portfolio mix of 60% stocks represented by Vanguard’s S&P 500 Index (ticker: VOO) and 40% bonds represented by iShares’ Core US Aggregate Bond Index (ticker: AGG). While we don’t default to a 60/40 for our clients, it serves as an illustrative common reference point across examples we provide.

Assume the same funds are available to an investor in both their Tax-Advantaged Accounts and their Taxable Accounts

Table 1: Yield and Tax Rates for High-Earning CA Couple For VOO and AGG

Vanguard S&P 500 Index (VOO)

iShares Core US Aggregate Bond Index (AGG)

30 Day SEC Yield1

1.16%

4.18%

Taxes on Yield:

Federal2

20.0%

37.0%

State3

10.3%

10.3%

NIIT4

3.8%

3.8%

Effective Tax Rate

34.1%

51.1%

1. As of August 31, 2025 for VOO and September 18, 2025 for AGG 2. Simplified assumption for this analysis that all VOO dividends are qualified while no distributions from AGG are qualified 3. CA levies flat 10.3% tax rate at this income level across all dividends and distributions 4. Assuming this couple will pay Net Investment Income Tax (NIIT) based on income

Optimizing Asset Location means taking into consideration two key traits of these assets that should be clear from the above:

First, qualified dividends from stock index funds such as VOO are generally taxed at a lower Federal rate than distributions from bond funds. For John and Jane’s income level that means a 20.0% rate for qualified dividends and 37.0% rate for bond fund distributions.

Second, the dividend yield of 1.16% on VOO is much lower than the 4.18% on AGG. In other words, there is less taxable income coming out VOO overall than AGG per dollar invested.

Our path to optimization is clear… move as much of the higher-taxed, higher-yielding asset into Tax-Advantaged Accounts (such as IRAs and 401k plans) while moving as much of the lower-taxed, lower-yielding asset into Taxable Accounts.

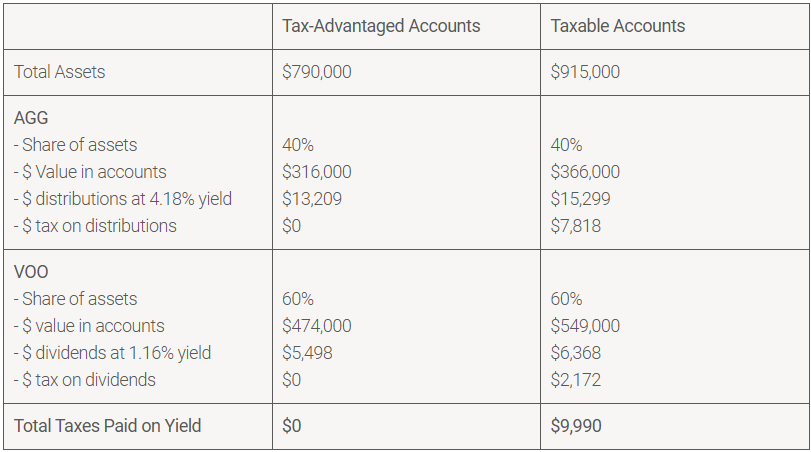

We’re going to assume John and Jane currently hold a 60% stock and 40% bond mix within each of their accounts which gives us the following split of assets and taxes between their Tax-Advantaged Accounts and their Taxable Accounts:

Table 2: Non-optimized, Consistent 60/40 Within Accounts:

Distributing assets in a 60/40 split consistently within each of their accounts results in John and Jane paying ~$9,990 in taxes on the dividends and distributions they receive from their investments.

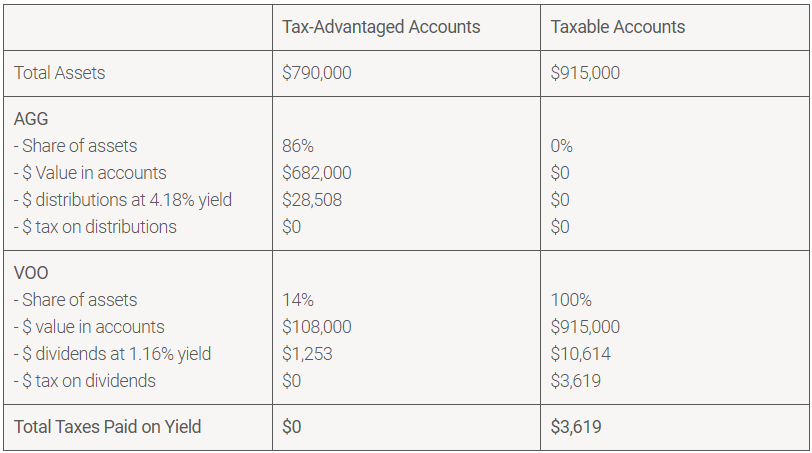

Now let’s look at what would happen if we optimize the portfolios for Asset Location by shifting as much of our bond mix into the Tax-Advantaged Accounts as we can while keeping the overall mix of stocks and bonds across accounts at 60/40. We’re making this shift because bonds both yield a higher income per dollar invested and are taxed at a higher rate than the stocks in our portfolio so we want to .

We now have the following results after redistributing assets across portfolios:

Table 3: Optimized, 60/40 Across Accounts

We’ve put all our bond holdings into the Tax-Advantaged Accounts boosting the share of bonds within those accounts to 86% (but keeping the total share of bonds across all accounts at 40%). We still have some stocks within our Tax-Advantaged Accounts, but our Taxable Accounts are now comprised 100% of lower yield, lower tax stocks. The total amount of pre-tax income we’re receiving from our investments in the form of dividends and distributions remains unchanged, but we’re keeping much more of the after-tax value of that income.

The net effect of this swap is a decrease in taxes paid on income from our investments from $9,989 a year down to $3,619. This is a decrease of $6,370 just by being a bit more intentional with how we approach allocating our assets across different types of accounts.

As we mentioned earlier, this is just a basic, illustrative example to show how more thoughtful asset location can benefit investors. In the real world, we would likely be doing this across a larger range of assets, account for the costs of reallocation, consider unique needs a client may have for a particular account, etc. Asset Location is also just part of our Systematic Enhancement approach to fully optimizing our clients’ investments.

Email us if you’d like to discuss anything in more detail or learn more about our services.

Disclosures: This content is for educational purposes only and is not an investment recommendation. This is not tax or legal advice. We receive no direct compensation from any of the funds discussed. Employees and clients of Kangpan & Co. may hold investments discussed in this article. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.

Wait, CLOs? That sounds vaguely like those things that blew a hole through the economy back in 2008… Close, but it was actually CDOs that contributed to the meltdown. According to VanEck’s William Skol:

“… not only did CLOs have nothing to do with the Global Financial Crisis, the asset class thrived through the 2008 crisis relative to other fixed income asset classes.”

Read on if you’re:

Looking for ways to increase yield in your portfolio without taking on significant credit risks

Interested in alternative credit options available in liquid forms

As a reminder, we are a fee-only fiduciary advisor and have no compensation arrangements with any of the funds discussed below.

A Quick CLO Primer

The love of TLAs (three-letter acronyms) within the financial world plays a part in this confusion between CDOs and CLOs. I spent a summer internship back in the mid-2000s structuring both these and other derivatives, and I still had trouble keeping all the acronyms straight as I was completing my rotation on the desk.

Collateralized Debt Obligations (CDOs) can be comprised of a variety of debt instruments including unsecured and junior obligations. It was sub-prime mortgage CDOs that played a dominant role in the 2008 collapse. We’re not going to cover CDOs any further in this post.

Collateralized Loan Obligations (CLOs) are a form structured credit that are generally backed by senior secured loans from corporate borrowers. Senior meaning first in line to be paid if a company experiences financial troubles. Secured meaning they are backed by the company’s assets.

The underlying loans within a CLO are also usually both liquid and tradable. Each CLO is generally made up of 150-250 individual loans. These loans are then further divided into a layered loss structure called “tranches” where losses are absorbed by each layer in a cascading sequence.

These layers are rated like other credit instruments from CCC (the riskiest) to AAA (the least risky). In order for AAA-rated CLO tranches to take a loss, all other preceding layers need to have blown out. This makes the AAA-rated CLO tranche a relatively lower risk investment vs. other corporate credit options out there.

I recommend checking out both the VanEck and BlackRock articles linked above for a more in-depth overview.

JAAA ETF Overview

CLOs have been around for decades now but only recently became available in a more easily accessible, liquid ETF form. They come in a variety of versions including those focused just on AAA-rated tranches which is what we’ll spend the rest of this post discussing.

There are multiple AAA CLO ETFs available (that’s three TLAs in a row if you’re keeping score), but we’ll use Janus Henderson’s (ticker: JAAA) for our analysis which is both the largest by AUM and the one that has been around the longest. Here’s a quick rundown of JAAA’s core attributes:

Beyond JAAA’s yield and performance, one of the most important characteristics of JAAA is its very low duration of 0.12 years which (a) gives this fund’s price very low interest rate sensitivity and (b) essentially makes this a floating rate investment.

We need to put JAAA’s performance in context by comparing against a benchmark asset. Here are a few key traits we need to consider when selecting a comparison asset:

A fixed income investment

Invested in AAA-rated credits or higher

With a very short duration

These attributes make the iShares 0-3 Month Treasury Bond ETF (ticker: SGOV) a solid contender to compare as the benchmark which is a fixed income product, invested in government debt, with a duration of just 0.09 years. Here are the attributes side-by-side:

A current yield spread of 120 bps and a persistent 134 bps increase in returns vs. short-term treasuries across time periods seems pretty good for a AAA-rated fixed income alternative with similar duration. So what’s the catch?

JAAA’s Historical Drawdowns

While the total return for JAAA has exceeded those of SGOV since JAAA’s launch, that return has come with a bit more volatility.

Unlike short-term treasury funds, short-term AAA CLOs ETFs can and have experienced notable drawdowns due to increased credit exposure and other factors. Let’s explore what these drawdowns have been.

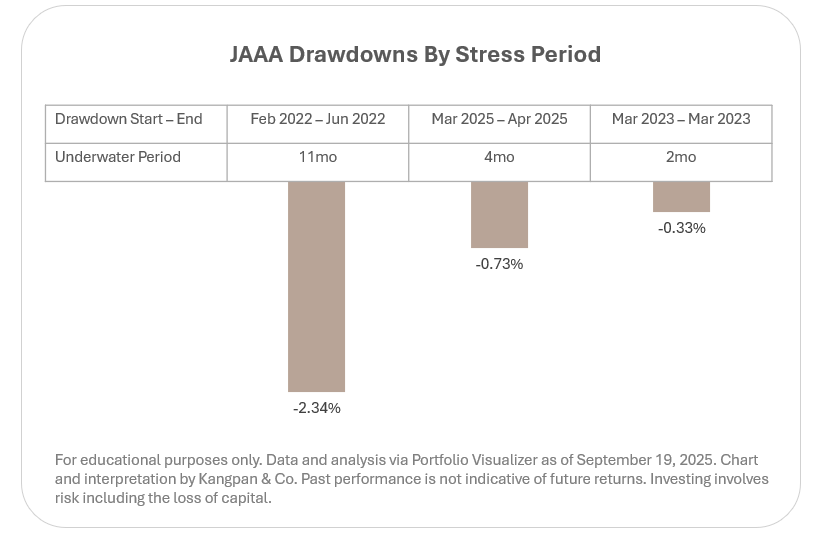

AAA CLOs have existed for decades but JAAA itself has only been around since October 2020. That means we can only look at a handful of stress periods to get a sense for how well it has held up. The chart below shows the three largest drawdowns for JAAA since launch with the following data points:

The start month of each drawdown and the end month when the lowest price was hit for that stress period

The Underwater Period which is the length of time between the drawdown start date to when when the investor fully recovered their initial investment inclusive of reinvested distributions

The max % total loss experienced (i.e. inclusive of distributions) during the drawdown

The largest drawdown was during 2022, aka the worst overall bond market since 1949 according to Bank of America and other bond analysts. JAAA’s drop during this time was primarily due to the aggressive rate hikes that resulted in a repricing of CLOs across the board along with increased trading activity among various market participants. However, it’s important to note that the relatively short Underwater Period of 11 months can be attributed to two key factors:

The very short duration of JAAA’s holdings which significantly reduces interest rate sensitivity as the holdings mature essentially making its holdings floating rate instruments so as the interest rates ratcheted up, the underlying holdings increased yields with less price impact than many other fixed income investments

The underlying changes to NAV were not due to credit issues given none of the holdings defaulted during this time (and, if you recall from earlier, no AAA CLO has ever defaulted as of the date of this post).

While by no means risk-free, we feel JAAA has held up fairly well under a relatively limited set of stress scenarios. That said, there are other considerations an investor should look into as well when assessing an investment like this such as tax implications, target interest rate exposure, etc.

Client Portfolio Strategy

Like many alternatives, AAA CLO ETFs aren’t necessary or even appropriate for every portfolio. Here are common situations where we think about utilizing these investments:

Clients with income-centric portfolios that want to enhance their yield within their short-term exposures without taking on significant credit risks

Clients with large cash and other liquid holdings that want to further enhance their yield for funds they are not anticipating needing within the next 1-2 years

There are other situations where we would consider including these liquid alternatives in portfolios based on client needs and risk tolerances which we help clients model out and understand the expected benefits and implications in doing so.

If you’d like to discuss anything in more detail, reach out to your dedicated advisor if you’re a current client or email us to learn more about our services.

Disclosures: This content is for educational purposes only and is not an investment recommendation. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.

Tax benefits are the primary reason many investors open 529 plans to save for education expenses. These mainly come in the form of:

Deferred taxes on the dividends, distributions, and growth of investments within the plan

Tax deductions from contributions made to the plan

The availability of, and rules for tax deductions from contributions vary significantly by your state of residence. We’ll be taking a look at the rules of a high-earner in New Jersey for this discussion.

High Earners May Not Be Eligible for State Tax Benefits

In New Jersey, up to $10,000 a year of 529 plan contributions are deductible from state taxes for residents contributing to the New Jersey 529 plan. However, this deduction is only available for those with a gross income of $200,000 or less.

That means if you’re a New Jersey resident who is fortunate enough to earn $200,000 a year or more, then you unfortunately do not get the benefit of the state tax deduction for contributions you make to a New Jersey 529 plan (though you still get the benefits of deferred taxes on the growth of your investments within the plan).

Compare Other 529 Plans If You Don’t Qualify For State Tax Benefits

It’s important to note not all 529 plans are created equal when it comes to fees and investment options. And you are generally not restricted to just using your state’s 529 plan. Let’s take a look at the potential fee benefits a high-earning New Jersey household could realize by moving their NJ 529 plan to another state’s plan such as California.

For this comparison we are looking at:

529 Plan State: the state where the plan is sponsored

Program Fees: asset-based fees charged by the plan administrator for managing the plan’s underlying investments

60/40 Fees: fund fees for implementing a 60% Stock / 40% Bond portfolio utilizing the options available within the plan. Fees for each individual fund are noted in parentheses

Yrly Fees Per $100,000: the expected yearly program and fund fees paid for every $100,000 invested in the plan

529 Plan State

Program Fees

60/40 Fees

Yrly Fees Per $100,000

New Jersey

0.10%1

0.046% blended – Franklin U.S. Large Cap Index 529 Portfolio (0.03%) – Franklin U.S. Core Bond ETF 529 Portfolio (0.07%)

$146 (0.146% total fees)

California

0.01%2

0.058% blended – Index U.S. Equity Portfolio (0.05%) – Index Bond Portfolio (0.07%)

$68 (0.068% total fees)

Data as of September 16, 2025 from each 529 Plan Sponsor’s Website 1. No fee for Franklin U.S. Government Money 529 Portfolio 2. For passive and index investment options

For every $100,000 invested in New Jersey’s 529 Plan, you are paying $78 more per year in fees vs. investing in a similar strategy within California’s 529 Plan. This may seem small but this could add up to thousands of dollars over the life of your 529 plan when you consider that you are a) paying this every year per and b) losing out on the power of compounding each time you pay the difference.

Remember, achieving your long-term financial goals is not about swinging wildly for the fences. It’s about making the small, disciplined choices each day that lead to a winning outcome.

If you’d like to discuss anything in more detail, reach out to your dedicated advisor if you’re a current client or email to learn more about our services.

Disclosures: This content is for educational purposes only and is not an investment recommendation. This is an illustrative example highlighting the difference in program and fund fees between two 529 Plans allocated to 60/40 strategies using available options. There are other considerations when selecting a 529 plan such as availability of investments, the expected performance of those investments, and other fees. The selection of California in this example is arbitrary and is not an endorsement of any specific plan. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital.

Investors often want to diversify their US-centric holdings with international stock exposure. A common question is which fund they should include and how much they should allocate. This piece will discuss our systematic process for selecting international funds along with which ones we prefer to recommend to clients based on portfolio goals.

INSIGHT Interestingly, we found Vanguard’s Total International Stock Index Fund (ticker: VXUS), one of the largest and most commonly recommended passive international index funds, came in 8th place using our aggregated, rank-ordered performance methodology. Spoiler alert, this is not one of our preferred recommendations.

As a reminder, we are a fee-only fiduciary advisor and have no compensation arrangements with any of the funds discussed below. These funds were chosen as our preferred options for clients as a result of our own objective research.

Our Process

We looked at more than 20 of the most popular International ETFs screening for funds that have at least five years of historical performance.

We pulled reported trailing market performance on September 1, 2025 from each of the fund’s web pages for 1, 3, 5 and 10 year periods (or whatever timeframe was the furthest available).

We then assigned a rank-order score to every fund within each performance time period. For example, IDMO was the best performer in the 3 year time period so it receives a rank-order score of “1”. IVLU was the 4th best performance in the 3 year time period so it receives a rank-order score of “4”.

Once each time period was rank-ordered, we then summed the scores across 1, 3, 5, and 10 year time periods to create a composite rank-order score. This final score allows us to sort for aggregated performance across all time periods, rather than focusing on a single one. It also provides an easier way to assess relative differences by looking at the numerical “distance” between the aggregate scores which we discuss a bit more below.

The chart above is a partial snapshot of our analysis. You can see that Invesco’s IDMO was a strong performer across all time periods which resulted in an aggregate score across every period of “7.” The second best performer across all time periods was iShares’ IVLU with an aggregate score of “20.”

This distance 13-point difference between IDMO and IVLU is significantly larger than the 2-point difference between IVLU and our third place performer. This is where the aggregated distance score helps us not only objectively rank-order the funds we assessed but also gives us a straight-forward heuristic to measure their relative differences.

Additional Considerations

Of course, just simply screening for trailing performance shouldn’t be the only consideration when selecting funds. We’re not short term performance chasers. We also look at other aspects of each fund including:

Fund Strategy: It shouldn’t be a surprise that we prefer simple, systematic strategies that are easily explainable and repeatable over purely discretionary decisions.

Stress Tests: We looked at the drawdowns during recent stress periods such as 2022’s stock and bond dual decline to understand how different funds held up under duress.

Correlations: We want an International strategy that provides some level of diversification from other major asset classes within a portfolio, especially vs. US Large Cap holdings.

A walkthrough of these additional analyses along with our full dataset are available to clients upon request.

Funds We Like

Here’s where we’ve landed after our assessment of the International ETF landscape. For clients that want:

Higher Returns with More Risk: Invesco’s International Momentum ETF (IDMO) had consistent outperformance across multiple time periods vs. most of the other funds we looked at. However, we also saw greater drawdowns during some of our stress test periods vs. IVLU and VYMI along with higher correlations to the S&P 500.

Diversificationand Less Volatility: iShares’ International Value ETF (IVLU) was our second-highest rank-ordered fund across time periods. Although slightly lower returns across time periods than IDMO, this fund also tended to exhibit better resilience during stress periods.

Income: Vanguard’s High Dividend International ETF (VYMI) was just short of having 10 years of trailing return data but ranked fairly well when looking across 1, 3, and 5 year time periods. The appeal is in it’s twelve month distribution yield which was approximately 3.90% as of September 12, 2025 – higher than the TTM yield on both IVLU’s 3.60% and IDMO’s 1.92%. That extra 30 bps of yield compared to IVLU equates to $3,000 more per year in pre-tax income for every $1,000,000 invested.

We incorporate International funds into many of our Core investment strategies and provide advice on how to add International exposure into portfolios on a project basis.

If you’d like to discuss anything in more detail, reach out to your dedicated advisor if you’re a current client or email us to learn more about our services.

Disclosures: This content is for educational purposes only and is not an investment recommendation. Speak with a licensed financial advisor before making any changes to your investments. Past performance is no guarantee of future returns. Investing involves risk including the loss of capital

Kangpan & Company LLC is a Registered Investment Advisor with the state of Pennsylvania. All content on this site is for educational purposes only and should not be considered financial advice. Past performance is not indicative of future returns and all investing involves risk including the loss of capital. Individualized responses to persons in a particular state will only be made after complying with all regulatory requirements of that state. Kangpan & Company LLC is not responsible for the content of external websites linked from this site. For a full description of our services, fees, and other important information, please read our Form ADV Part 2A, which are available on the SEC’s website here.